📊 Full opportunity report: The bank account in the chat. How personal finance became an agentic on-ramp. on ThorstenMeyerAI.com — validation score, market gap, and execution plan.

TL;DR

OpenAI’s ChatGPT now allows Pro users in the US to connect bank accounts and financial data, marking a step toward agentic finance tools. This development could reshape consumer-finance interactions over the next two years.

OpenAI has launched a preview of personal-finance tools within ChatGPT for Pro subscribers in the United States, allowing users to connect bank accounts, credit cards, and investment accounts through Plaid. This development marks a significant step toward integrating agentic financial services directly into the chat interface, potentially transforming how consumers interact with financial products and services.

The new feature enables users to link accounts from over 12,000 financial institutions, including Chase, Fidelity, Schwab, Robinhood, American Express, and Capital One. Once connected, ChatGPT provides a dashboard displaying spending, portfolio performance, subscriptions, upcoming payments, and answers grounded in real-time account data. The launch leverages OpenAI’s latest reasoning model, GPT-5.5, evaluated at high performance levels by internal benchmarks and finance professionals. While the current preview is read-only, OpenAI has announced forthcoming integration with Intuit, which will enable agentic tasks such as credit card applications, tax filings, and scheduling with financial advisors. Over 200 million people already ask ChatGPT personal finance questions monthly, according to Plaid’s CTO, and OpenAI emphasizes that the current tool is not a substitute for professional advice but a trust on-ramp for more advanced, agentic features coming soon.The bank account

in the chat.

How personal finance

became an agentic

on-ramp.

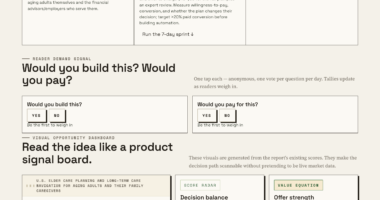

arriving at ChatGPT (pre-launch)

connectable via Plaid

internal finance benchmark

credit card flow first · Intuit

analytical layer

- Balance retrieval across accounts

- Transaction analysis + categorization

- Pattern identification over time

- Planning scenarios with grounded data

- Dashboard rendering + financial memories

on-ramp →

product

execution layer

- Credit card application + approval odds (Q1 2027)

- Tax filing flow via Intuit · 2027 tax season

- Advisor scheduling · routed to live experts

- Investment trades · partnership-mediated

- Bill payment + savings switching · 2027-2028

The read-only preview is the trust on-ramp. The agentic version is the actual product. What gets unbundled is not the feature; it is most of the consumer-fintech intermediation stack built over the past 25 years — and the intermediation moves up the stack to the chat layer.Thorsten Meyer · The Bank Account in the Chat · Agentic Commerce 01

Transforming Consumer-Finance Interaction via ChatGPT

This launch signals a structural shift in consumer fintech, where the chat interface becomes the primary on-ramp for financial services. By connecting accounts and providing real-time insights, ChatGPT could reduce reliance on traditional financial apps and intermediaries, re-pricing the downstream ecosystem of banks, brokerages, and fintechs. The move towards agentic capabilities—such as submitting loan applications or scheduling financial advice—may redefine the relationship between consumers and financial institutions, impacting industry dynamics, trust frameworks, and regulatory approaches over the next two years.As an affiliate, we earn on qualifying purchases.

From Personal Finance Management to Agentic Finance

For over a decade, personal finance management (PFM) apps have aimed to simplify financial oversight through dashboards and data aggregation. However, the emergence of conversational AI with live account access shifts this paradigm. Prior to this launch, ChatGPT was used mainly for questions without account context, with an estimated 200 million monthly queries about personal finance. The recent integration with Plaid introduces a new surface where the chat layer becomes the primary interface for financial decision-making, setting the stage for a broader move toward agentic financial services. This transition is also influenced by evolving regulatory frameworks, notably the differences between US and European open banking architectures, which may affect how these tools develop internationally.“More than 200 million people already ask ChatGPT personal-finance questions every month.”

— Plaid CTO

Money Skills for Young Adults: A Beginner’s Guide to Smart Financial Habits, with Simple Tools to Manage Your Budget, Save for Goals, Invest, and Build Your Independent & Secure Future

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

Unclear Aspects of Regulatory and International Expansion

It is not yet clear how European regulatory architectures—such as PSD2, PSD3, and FIDA—will influence or reshape the deployment of similar features outside the US. The US rollout’s path to Europe will likely involve re-architecting infrastructure and compliance models, but specific timelines and regulatory acceptance remain uncertain. Additionally, the full scope of agentic capabilities and how they will be integrated into existing financial ecosystems is still developing, with some features announced but not yet operational.

Funded Futures Performance Journal: Institutional Trade Log, Risk Management Dashboard, Psychology Tracker & Funded Account Growth System

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

Next Steps in Consumer-Finance Integration and Regulation

OpenAI plans to expand the feature to include integrations with Intuit, enabling tasks like credit card applications, tax filings, and appointment scheduling within the next 12 to 24 months. Regulatory developments, especially in Europe, will influence how these tools evolve and are adopted internationally. Industry stakeholders are watching closely to see how the agentic layer impacts downstream financial services, pricing, and consumer trust, with ongoing discussions about regulation, safety, and competitive dynamics.

Ultra Large Format Monthly Bill & Expense Tracker: Plan, Track, Save!: Senior-Friendly Design with Debt and Subscription Trackers, Savings Challenges, … (The Complete Financial Tracker Series)

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

Key Questions

Will this feature replace traditional banking apps?

Currently, the feature is a read-only preview designed to build trust and demonstrate capabilities. Full agentic functions are expected in future releases, which could reduce reliance on traditional apps, but this transition is still in development.

How secure is linking my bank account to ChatGPT?

OpenAI uses Plaid, a trusted financial data aggregator, to connect accounts, and the process follows existing security protocols. However, users should remain cautious and aware of privacy considerations when sharing financial data.

Will this be available outside the US?

The current rollout is limited to the US. European and other international markets will require adaptations to local regulations and infrastructure, which are still under discussion.

What kinds of tasks will agentic capabilities include?

OpenAI has announced future capabilities such as submitting loan applications, scheduling appointments, and filing taxes, but these are not yet available.

Source: ThorstenMeyerAI.com